The planned initial public offerings this year of SpaceX, Anthropic and OpenAI comprise over $3 trillion in estimated value. In addition, a host of smaller (but still large cap) names such as Databricks, Stripe and Anduril are expected to go public soon. This influx of mega-cap names will reshape equity benchmarks, but the immediate impact will be limited until the sale restrictions for private investors (typically 180 days) expire.

A defining feature of this cycle is the expected limited public float at the time of listing. While indexes such as the S&P 500 or Russell 1000 are referred to as market capitalization-weighted (market capitalization equals the total value of all the outstanding shares), in reality they are float-weighted. Float refers to the aggregate value of shares that can be freely traded, which excludes restricted insider shares and shares subject to post-IPO lockup. In the case of SpaceX, shares available for public trading may represent less than 5% of total equity value. At this level, the company would fall below the thresholds required for immediate inclusion in major indices such as the S&P 500 and Russell 1000. While this outcome may appear counterintuitive given the company’s scale, index providers rely on float-adjusted market capitalization and liquidity metrics rather than headline valuation.

This distinction introduces a dynamic that differs from prior cycles. Rather than a single event, index inclusion becomes a multi-stage process, driven by the expiration of lockups and the gradual increase in publicly available shares. As float expands, eligibility is established, index weights increase, and passive funds are required to allocate capital accordingly. The result is a delayed but persistent flow of demand, which may exert a more meaningful influence on pricing than the IPO itself.

At the same time, index providers are reevaluating eligibility criteria. Proposals to reduce seasoning periods and ease profitability requirements reflect the challenges posed by very large, but often unprofitable, issuers. While these changes may accelerate inclusion timelines, they do not alter the underlying reliance on float-adjusted weightings.

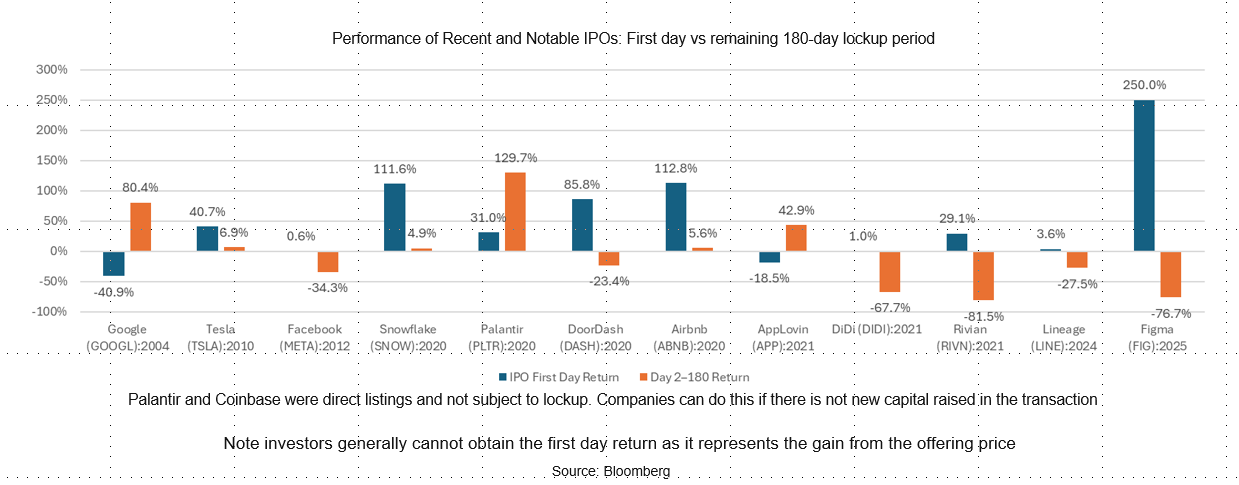

Periods of innovation often bring renewed enthusiasm and, at times, a degree of extrapolation. While the underlying technologies driving these businesses are transformative, the distinction between economic importance and investability remains critical. The generally poor performance of IPOs after the first trading day illustrates the importance of economic fundamentals over hype:

Initial public offerings have typically generated strong first-day returns, largely captured by investors participating directly in the offering. Subsequent performance during the lockup period has been more muted, and in many cases negative. For most investors who access shares in the secondary market, realized returns often differ materially from the gains implied by initial pricing.

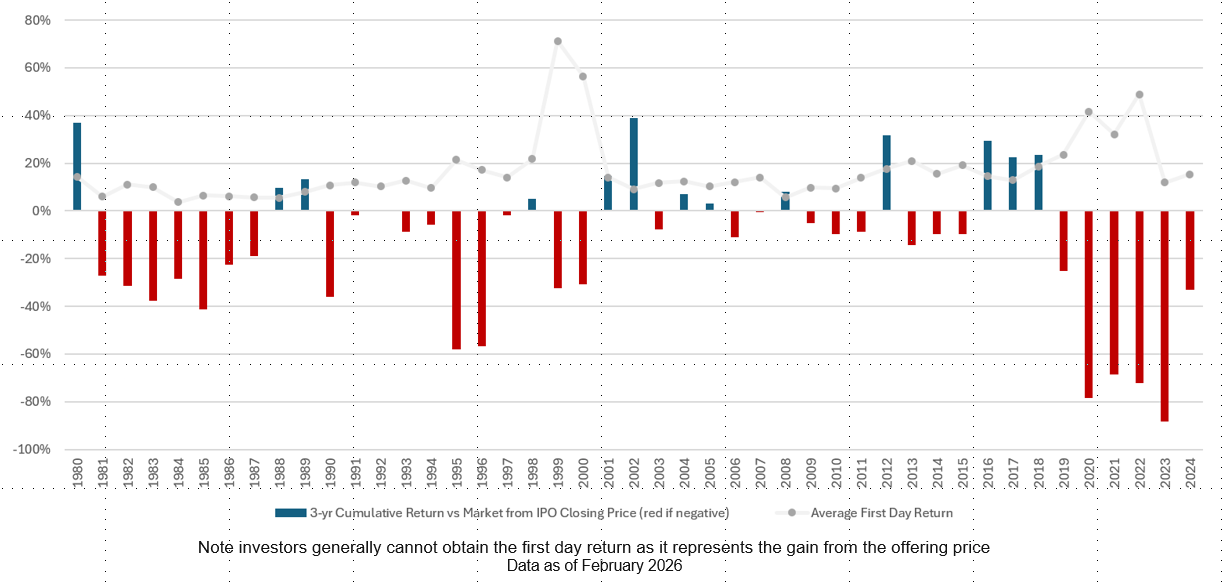

IPOs tend to underperform over the three-year period after the first-day return

Over longer horizons, IPOs as a group underperformed broader equity markets1. This underperformance reflects a combination of elevated valuations at issuance, the monetization of early investor stakes, and a gradual normalization of expectations following the transition to public ownership.

Implications for Portfolio Construction

Passive strategies, by design, must respond to index changes as they occur. As float expands and index weights increase, passive funds are required to purchase shares irrespective of valuation. This creates a price-insensitive source of demand, often occurring after significant appreciation has already taken place. In this way, index construction can introduce a pro-cyclical, momentum-driven element to portfolio allocation.

Active managers, by contrast, retain discretion over timing and position sizing. The staged nature of float expansion may present opportunities to initiate or adjust positions under more favorable conditions, particularly following lockup expirations when additional supply enters the market. Our equity managers have typically avoided early investments in IPOs, waiting for them to be seasoned and demonstrate that the business model can deliver sustained growth.

Valuation also remains an important consideration. SpaceX could go public trading at around 100 times revenue – a staggeringly high valuation that assumes years of very high growth and creates risk of large declines if growth disappoints. OpenAI and Anthropic are growing revenues but have yet to demonstrate profitability.

The scale of these offerings may also influence broader market liquidity. Large capital raises can absorb a significant amount of investor demand, potentially delaying or crowding out activity in other segments of the market.

Maintain Discipline in a Changing Environment

As in prior periods of innovation, investors should avoid chasing compelling narratives and apply a consistent, disciplined investment framework. Narratives surrounding transformative technologies and high-profile companies can shift rapidly. Attempts to anticipate these shifts or time market entry points often prove less reliable than a focus on diversification, valuation awareness, and long-term objectives. Investors are best served by portfolios constructed to meet long-term cash flow needs while managing risk across a range of economic outcomes. This approach emphasizes resilience over opportunism and seeks to avoid the permanent loss of capital that can result from concentrated exposures or reactive decision-making.

Disclosures

This information is presented for educational purposes only and does not constitute an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. Past performance is not indicative of future results.

Equity securities will fluctuate in value, and such fluctuations may result in losses. Fixed income investments are subject to interest rate, credit, and liquidity risks. Alternative investments involve additional risks, including limited liquidity and greater volatility.

Index performance is shown for illustrative purposes only and is not available for direct investment. Investors should consult with their financial advisor and/or tax professional before implementing any strategy discussed herein.

- Ritter, J. R. (2026). Long-run Returns on Initial Public Offerings. University of Florida, Warrington College of Business. https://site.warrington.ufl.edu/ritter/files/IPOs-long-run-returns-on-IPOs.pdf

↩︎