This information is presented for educational purposes only and does not constitute an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein. Past performance is not indicative of future performance.

Election Impact on Financial Markets

The Republican victory on Tuesday delivered a second term for Donald Trump and majorities in both houses of congress (as of this writing the House is still undetermined but leaning Republican). As incumbents tend to lose seats during mid-term elections, this majority may only last through 2026. President Trump will likely utilize his congressional advantage more effectively than he did in the first two years of his first term, with his focus on tax and trade policy providing the greatest impact on financial markets.

Equity Performance from Nov 1-8

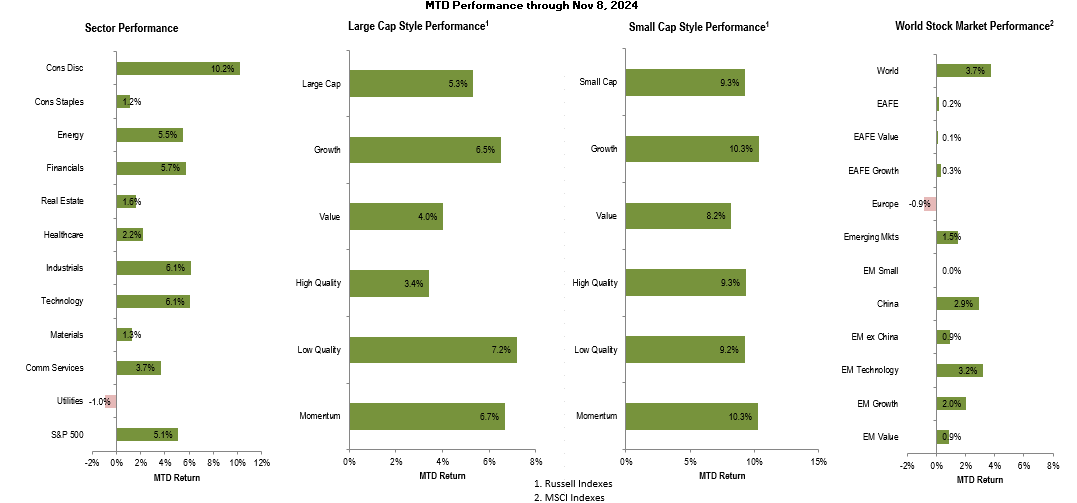

Small Caps led the Post-Election Rally

Small-cap US stocks surged after the election, with the Russell 2000 index rising nearly 6% the next day and up 9.3% in the first week of November. Treasury bonds declined, with yields on the 10-Year increasing by 16 basis points and the inflation breakeven on 5-year TIPS (the inflation rate at which TIPS outperform nominal Treasuries) increasing by nearly 20 basis points. Earnings season, Thursday’s Fed announcement of the expected 25 basis point cut, and new rounds of Chinese government stimulus also impacted markets this month, making it difficult to draw too fine a conclusion on the election’s impact.

Tax, Trade and Regulatory Policy favor Business

A major uncertainty for American businesses has been the expiration of key provisions of the Tax Cuts and Jobs Act of 2017. While the current corporate tax rate of 21% does not sunset, the Democrats indicated a desire to increase taxes on businesses. The 20% deduction for qualified pass-through income (199A), which applies to REITs, S-Corps and other flow-through vehicles will terminate at the end of next year. Investors benefited from this treatment, and it will likely now be extended. Rules around accelerated depreciation, which allowed companies to fully depreciate certain investments in the year of purchase, began to step down in 2023 and will expire in 2025. The renewal of this would incentivize companies to invest and this would provide further support to small cap stocks.

The administration’s trade policies will further the current trend of deglobalization and American reindustrialization. Programs will likely include a national security component due to embarrassment over a lack of arms manufacturing capacity, exemplified by Russia producing three times more artillery shells than the US and Europe for the war in Ukraine. The administration may attempt another trade agreement with China, after Trump’s 2020 deal that contained largely symbolic purchases of US goods. Trump’s friendly relations with Indian president Narendra Modi and their common wariness of China increases the potential for an increased trading relationship.

We can also expect regulatory policies to favor business. Energy and industrial stocks rallied after the election. A more favorable anti-trust policy may trigger more corporate acquisitions, particularly among private equity. Stocks associated with green energy sold off. However, economics more than policy drives the current mix of natural gas, wind and solar for electricity generation.

Higher Inflation Risks

While the Republican victory buoyed markets, it also increased the risk of inflation. The cost of tariffs will likely be passed on to American consumers. Budget deficits may scare away investors in US government bonds, prompting higher interest rates. The term of current Fed chairman Jerome Powell, whose record rate hikes stemmed inflation, ends in May 2026. Trump’s expressed preference for low interest rates will likely result in a more dovish replacement who may find it difficult to employ as stringent anti-inflation measures should they become necessary.

Diversification Remains Essential

While we mostly agree with the market’s take on the election, financial markets often manage to find a way to frustrate expectations. Small cap US stocks lagged over the past decade and now trade at record valuation discounts to the S&P 500. Cheap valuations combined with policy support and improving sentiment bode well for the asset class. However, these stocks are also most vulnerable to a recession, so disciplined allocation remains essential. Deglobalization and the risk of volatile US policy changes may also increase the benefits of international diversification.